- Topic

9k Popularity

8k Popularity

164k Popularity

22k Popularity

20k Popularity

- Pin

- Gate July 2025 Transparency Report:

Accelerating Leadership in the Global Crypto Landscape!

#GateTransparencyReport# - 📢 Gate Square Exclusive: #PUBLIC Creative Contest# Is Now Live!

Join Gate Launchpool Round 297 — PublicAI (PUBLIC) and share your post on Gate Square for a chance to win from a 4,000 $PUBLIC prize pool

🎨 Event Period

Aug 18, 2025, 10:00 – Aug 22, 2025, 16:00 (UTC)

📌 How to Participate

Post original content on Gate Square related to PublicAI (PUBLIC) or the ongoing Launchpool event

Content must be at least 100 words (analysis, tutorials, creative graphics, reviews, etc.)

Add hashtag: #PUBLIC Creative Contest#

Include screenshots of your Launchpool participation (e.g., staking record, reward - 🎉 Hey Gate Square friends! Non-stop perks and endless excitement—our hottest posting reward events are ongoing now! The more you post, the more you win. Don’t miss your exclusive goodies! 🚀

🆘 #Gate 2025 Semi-Year Community Gala# | Square Content Creator TOP 10

Only 1 day left! Your favorite creator is one vote away from TOP 10. Interact on Square to earn Votes—boost them and enter the prize draw. Prizes: iPhone 16 Pro Max, Golden Bull sculpture, Futures Vouchers!

Details 👉 https://www.gate.com/activities/community-vote

1️⃣ #Show My Alpha Points# | Share your Alpha points & gains

Post your - 💙 Gate Square #Gate Blue Challenge# 💙

Show your limitless creativity with Gate Blue!

📅 Event Period

August 11 – 20, 2025

🎯 How to Participate

1. Post your original creation (image / video / hand-drawn art / digital work, etc.) on Gate Square, incorporating Gate’s brand blue or the Gate logo.

2. Include the hashtag #Gate Blue Challenge# in your post title or content.

3. Add a short blessing or message for Gate in your content (e.g., “Wishing Gate Exchange continued success — may the blue shine forever!”).

4. Submissions must be original and comply with community guidelines. Plagiarism or re

[Forex] Implications of the Surge in Stock Prices on US-Japan Monetary Policy | Yoshida Tsune's Forex Daily | Moneyクリ Monex Securities' Investment Information and Media Useful for Money

Possibility of BOJ Rate Hike Being Brought Forward Due to Surge in Japanese Stocks

This week, the Nikkei average has surged, significantly surpassing the all-time high recorded in July 2024 (see Chart 1). Stock prices are generally considered one of the leading indicators of economic conditions. Such movements in stock prices reaching new highs could be a factor that brings forward the resumption of interest rate hikes by the Bank of Japan.

[Figure 1] Nikkei Average Trends (January 2024 onwards) Source: Created by Monex Securities from data provided by Refinitiv.

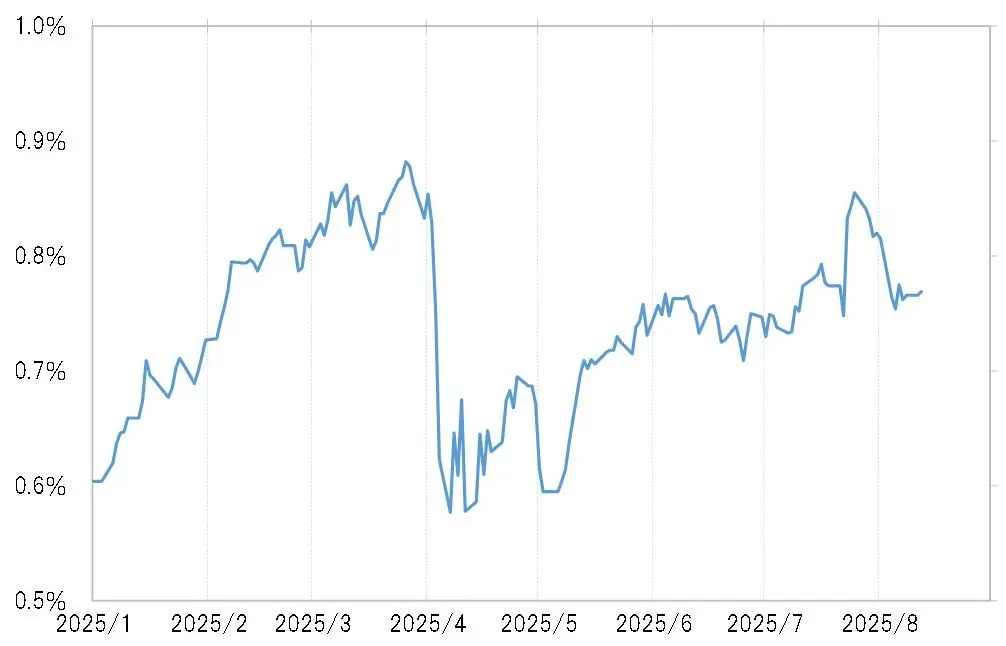

The Bank of Japan decided to implement additional interest rate hikes in January 2025, and subsequently showed a strong desire for further rate increases. Reflecting this monetary policy, the 2-year bond yield rose to nearly 0.9% by March (see Figure 2). However, in April, when U.S. President Trump announced reciprocal tariffs, a global stock market crash occurred, leading to a "tariff shock," which forced a reassessment of the Bank of Japan's additional rate hike scenario.

Source: Created by Monex Securities from data provided by Refinitiv.

The Bank of Japan decided to implement additional interest rate hikes in January 2025, and subsequently showed a strong desire for further rate increases. Reflecting this monetary policy, the 2-year bond yield rose to nearly 0.9% by March (see Figure 2). However, in April, when U.S. President Trump announced reciprocal tariffs, a global stock market crash occurred, leading to a "tariff shock," which forced a reassessment of the Bank of Japan's additional rate hike scenario.

[Figure 2] Trends in Japan's 2-Year Bond Yield (January 2025 onwards) Source: Created by Monex Securities from data provided by Refinitiv.

At the monetary policy meeting held on July 31, when stock prices were recovering, no additional interest rate hike was decided, and at the press conference after the meeting, Bank of Japan Governor Ueda mentioned that he still wanted to assess the impact of the tariff increases. However, considering that stock prices surged afterward, there is a possibility that they may consider an additional interest rate hike at the next monetary policy meeting on September 19.

Source: Created by Monex Securities from data provided by Refinitiv.

At the monetary policy meeting held on July 31, when stock prices were recovering, no additional interest rate hike was decided, and at the press conference after the meeting, Bank of Japan Governor Ueda mentioned that he still wanted to assess the impact of the tariff increases. However, considering that stock prices surged afterward, there is a possibility that they may consider an additional interest rate hike at the next monetary policy meeting on September 19.

Could the pressure to correct the yen's depreciation from the U.S. also affect the Bank of Japan's rate hike?

There is a possibility that the Bank of Japan is also conscious of the pressure from the Trump administration, which is requesting the correction of the weak yen, regarding additional interest rate hikes. This is because there was a mention in the currency report published by the U.S. Treasury Department at the beginning of June.

"Taking into account the growth of the Japanese economy and inflation trends, the Bank of Japan has been tightening monetary policy since 2024, and this should continue in the future," he said, adding, "Such actions will normalize the depreciation of the yen and the appreciation of the US dollar, as well as lead to a desirable structural rebalancing of bilateral trade."

Possibility of Japan-US "Monetary Policy Coordination" in September = Consideration for Yen Depreciation Correction?

On the other hand, in the United States, concerns about a sharp deterioration in the labor market have emerged following the release of the U.S. employment statistics on August 1. This has led to speculation about the possibility of the Fed resuming interest rate cuts. Ahead of the next FOMC (Federal Open Market Committee) meeting on September 17, some voices are expecting a significant rate cut of 0.5%.

However, it is unnatural to hastily resume rate cuts while stock prices, which are leading indicators of the economy, are surging (see Chart 3). Within the FRB, there seems to be concerns about the resurgence of inflation due to increased tariffs, but rising stock prices fundamentally also pose a risk of reigniting inflation. Considering the above, the recent surge in stock prices may lead the FRB to be cautious about resuming rate cuts.

[Figure 3] NY Dow Trends (January 2024 - ) Source: Created by Monex Securities from data by Refinitiv.

However, due to President Trump's blatant demands for interest rate cuts, it seems increasingly difficult for Chairman Powell of the Fed to refuse them objectively. In this context, if a rate cut is decided at the FOMC on September 17, then, as mentioned above, the Bank of Japan's interest rate hike on September 19 could result in the possibility of cooperation in monetary policy between Japan and the United States.

Source: Created by Monex Securities from data by Refinitiv.

However, due to President Trump's blatant demands for interest rate cuts, it seems increasingly difficult for Chairman Powell of the Fed to refuse them objectively. In this context, if a rate cut is decided at the FOMC on September 17, then, as mentioned above, the Bank of Japan's interest rate hike on September 19 could result in the possibility of cooperation in monetary policy between Japan and the United States.

The coordinated monetary policy where the financial policies of Japan and the United States move in opposite directions at almost the same time was implemented in July 1995 to correct the depreciation of the US dollar and the appreciation of the yen. This time, the direction of the exchange rate is the opposite, but due to the Bank of Japan's interest rate hike and the Federal Reserve's interest rate cut, the interest rate differential between Japan and the US (US dollar advantage and yen disadvantage) may significantly narrow, which could potentially lead to a correction of the US dollar's strength and the yen's weakness.